Rise of the designer founder

Let's start a riot

If you’re new to the games industry, it’s hard to grasp just how much the fundraising landscape has changed in recent years, particularly for studio founders.

In the past, VCs did invest in games, including storied firms like Accel, Kleiner Perkins and Benchmark. Europe also had a number of influential players, especially at seed. But especially for companies that were in the business of making games, funding options were limited.

All that has changed. There are now dozens of dedicated funds, generalist firms have hired gaming-focused partners, and multiple strategic investors (many from Asia) are active at every stage from seed through acquisition.

This influx of capital has resulted in a substantial increase in studios getting funded. For anyone who wants to see more high quality and ambitious games getting made, this is unquestionably a good thing.

One result of this has been a phenomenon we could call the rise of the “designer founder”. I define this as someone who has played a senior creative role on a significant franchise at one of a handful of well-known large game companies, who is now leaving to start a new studio.

What Mitch calls “pedigree chasing” is unquestionably a Thing in gaming venture capital.

I think there are a few reasons for this. Though VCs profess their affinity for the crazy ones, the truth is that many come from conventional highly credentialed backgrounds, and think of companies like Riot, Epic and Blizzard as the games industry equivalent of Stanford, Harvard and Yale. When a company is not much more than a pitch deck and a few entries on a cap table, putting money behind brand names feels safer.

Is it safer? It’s too early to tell - games take a long time to get to market - but we will learn a lot about the returns on this strategy over the next few years.

In the meantime, I think there are some important things to consider when evaluating founders, particularly ones from this background.

Do a real “credit check”

Experience matters, of course. But the kind of experience matters much more.

The 0-to-1 experience of leading a game from concept through prototyping, pre-production, production, launch and post-launch is much more relevant to the startup studio journey than working on a project that already has momentum from an established brand, audience and team.

Here’s the problem, though. By definition, almost no-one has had the opportunity to build something big from scratch (the precious few that have can write their own tickets). Places like Riot and Blizzard are magnets for creative talent, but how can you assess what they really did?

Any games investor worth their salt should have a network of highly trusted insiders at each of these companies who can give you a real backchannel reference check. These conversations can be incredibly revealing, and it’s surprising how many don’t do them.

A final question to consider on this topic: has the team shipped games together before? This is both more valuable than individual founder pedigree, easier to assess and perhaps more indicative of future potential.

Can they go to market?

As Mitch points out, the founders of the Ivy League companies did not have this pedigree. So, what else matters?

I strongly believe in the value of having go-to-market DNA in the founding team -someone who, from inception, is figuring out how to build an audience. This is doubly true for founders transitioning from larger companies which have extensive marketing infrastructure and massive incumbent advantages.

In a startup, even a well-funded one, that support doesn't exist. It’s important to have this in the founding team’s DNA not only because this has to be a priority from the very start, but also because that person needs to have enough influence to meaningfully impact the product itself. The history of games is littered with the corpses of auteur game designers who were given the unfettered freedom to make whatever they wanted, audience be damned.

Are they audience driven or vision-driven?

This leads neatly to my next consideration: the ability to reconcile being vision-driven with audience-driven. Vision-driven creators are fueled by an intuitive, creative impulse to materialize something they want to see in the world. However, it's equally important to be audience-driven – relentlessly testing assumptions to ensure you're building something people want.

There are vanishingly few creators whose genius you can trust enough to be fully vision-driven: Jenova Chen, Will Wright, Sid Meier perhaps? But part of the genius of these designers is that they are thinking deeply from first principles about the audience and how they can create something that serves them in a unique way.

For everyone else, I think it’s important to be paranoid about validating your creative assumptions. For more on what that looks like, I highly recommend listening to this interview of Slim and Trevor (who led the development of Valorant while at Riot) from Raid Base on how they approach making their game.

Can they operate under startup constraints?

Startups are an exercise in doing more with less, and figuring out what really matters. If you’re coming from an environment where $100M budgets are the norm, you might think taking “only” $30M to get to market is cheap. There are firms that can finance these budgets (and more), but here’s a final thought to ponder.

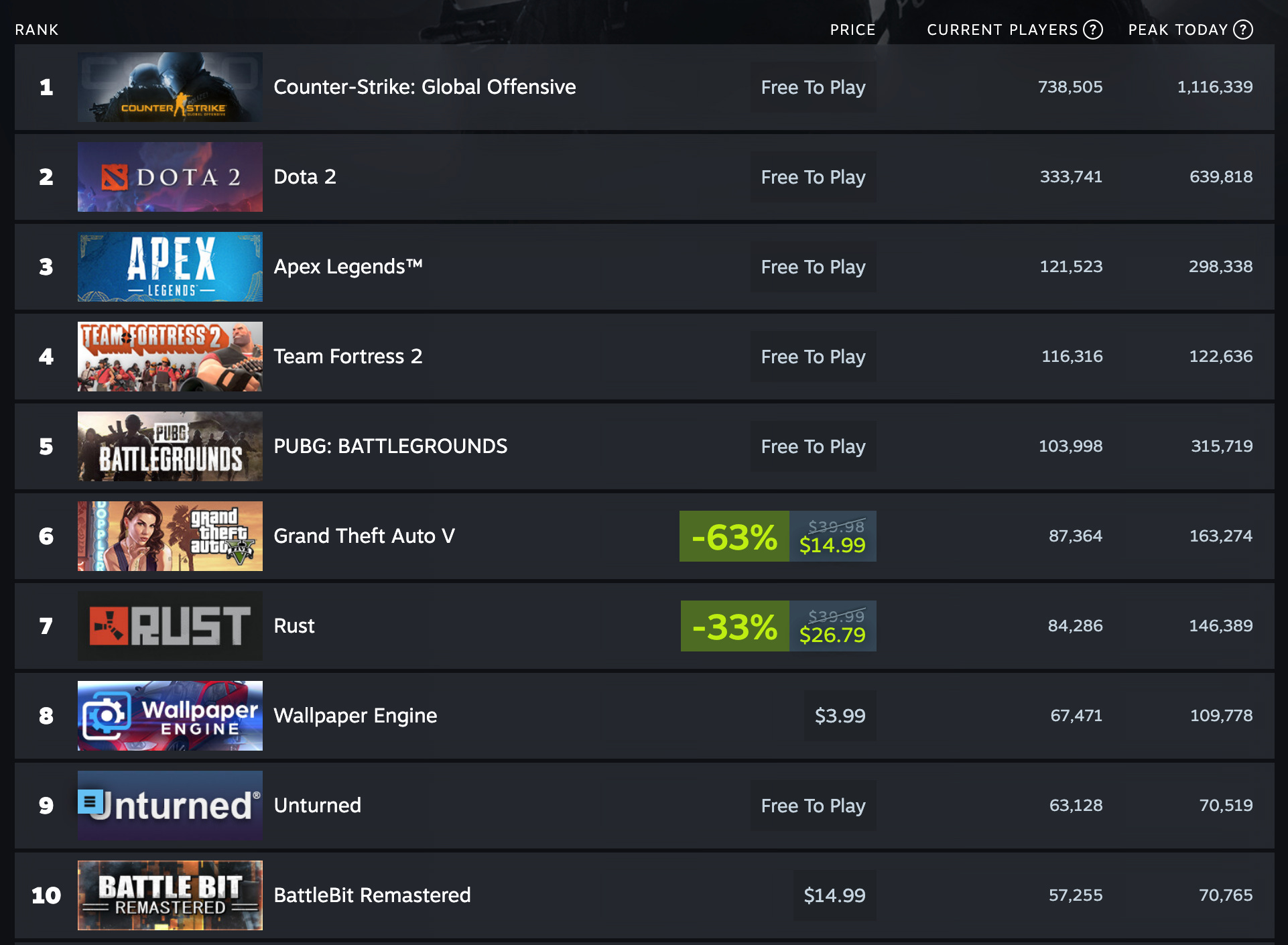

As my friend Justin Yuan points out, 2 of the top 10 most played games on Steam right now are low poly games made by small teams.

There are many paths to success, and I suspect the best returns will come from the ones less trodden.

Thanks to Joakim Achrén, Eric Kenna, Justin Yuan and Mitch Lasky for reading and providing feedback on drafts of this essay.

David Kaye is co-founder and General Partner at F4 Fund. If you are raising for a pre-seed or seed-stage games or technology company, please reach out. Getting an intro from a founder we know is best, but a well-written cold email works too.

Does anyone have names for what the author refer to as

"There are now dozens of dedicated funds, generalist firms have hired gaming-focused partners, and multiple strategic investors (many from Asia) are active at every stage from seed through acquisition."

I feel the author is holding back on that info , being an investor himself